Global approaches to nus procurement and industrial policy

The production of complete buses involves a web of interconnected suppliers and manufacturers, covering components from steel to semiconductors to skilled labour and logistics networks, News.az reports, citing Bus News Magazine.

RECOMMENDED STORIES

Within this system, government funding plays a critical role in stabilising supply chains, enabling technology adoption and incentivising domestic production.

In the US, agencies like the Federal Transit Administration (FTA) distribute grants to state and local transit authorities, enabling them to procure new buses. For example, in November 2025, the FTA invested 2 billion USD in 2,400 buses and improvements to bus infrastructure. Such funding creates predictable demand for manufacturers, allowing companies to plan production cycles, invest in capacity, and maintain long-term supplier relationships. Without a steady pipeline of orders, manufacturers face volatile demand, which could disrupt suppliers and increase costs.

Notably, regulatory requirements mandate that these funds are used in alignment with “Buy America” standards, ensuring that steel, iron, and manufactured products are produced in the US. Specifically, the funded buses must have at least 70% domestic content and undergo final assembly in the United States if the project is valued at over 150,000 USD. This ensures that federal funding supports domestic manufacturing, jobs, and supply chains.

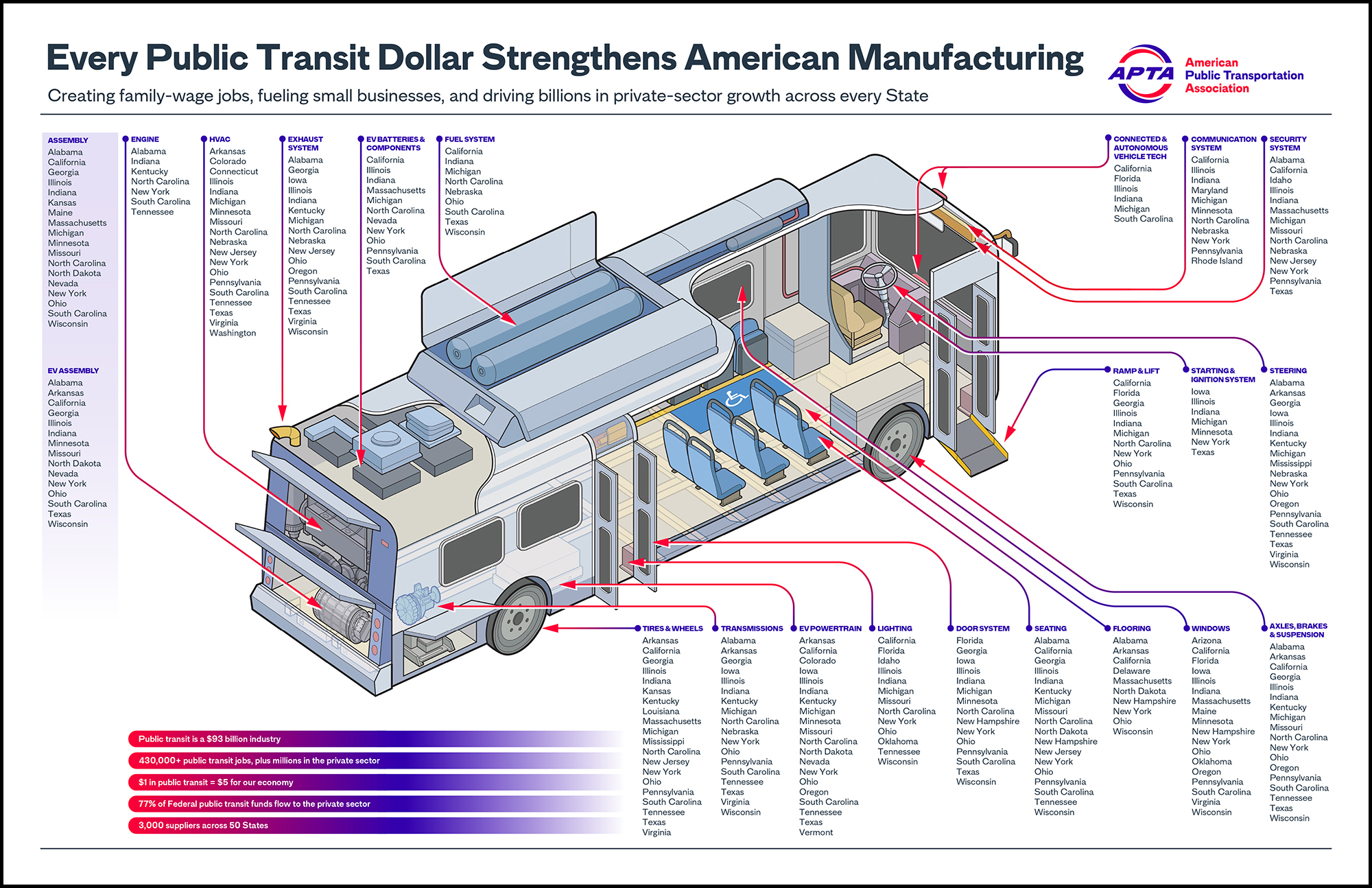

Highlighting the benefits of these policies, the American Public Transportation Association (APTA) reports that about 77 percent of federal public transit funding flows to private-sector companies, supporting manufacturing activity and family-wage jobs across the country.

To illustrate the spread of this supply chain, APTA has also released a manufacturing schematic for the bus industry. This visual maps where different components are produced and identifies the states involved. For example, nine states (California, Indiana, Michigan, North Carolina, Nebraska, Ohio, South Carolina, and Texas) are shown to produce components for bus fuel systems. Overall, the research identified over 3,000 suppliers across 50 states, supporting millions of jobs.

However, the implications of these regulatory requirements are not without challenges. Compliance with “Buy America” standards can increase production costs, particularly for components that are more readily available or cheaper from international suppliers. This can stall development in transit networks by driving up costs and creating bottlenecks in procurement timelines due to the limited number of compliant suppliers. In contrast, in countries without these requirements, agencies can access a more open pool of bidders, leading to healthy competition and the potential for more cost-effective and optimal solutions.

Recognising these constraints, the Federal Transit Administration (FTA) has proposed waivers of Buy America requirements for specific products, including battery‑electric minibuses. This phased waiver was proposed in late 2024, as fully compliant zero‑emission buses were not yet widely available in the US market. Such considerations thus underscore the practical challenges of balancing domestic procurement standards with the rapid adoption of emerging technologies.

Comparison with the European Market

The challenge of rapid technology adoption is particularly significant in Europe, where the European Union has mandated that 90 percent of all new city buses must be zero‑emission by 2030, rising to 100 percent by 2035. To meet these targets, operators are procuring buses at a pace and scale that domestic manufacturers cannot meet. Consequently, a growing share of orders has been filled by overseas producers, with Chinese vehicles from companies such as Yutong and BYD currently making up around a third of Europe’s bus fleet.

As a result of this shift, European manufacturers and their subsequent supply chains are facing increased pressure. Volvo closed its Wroclaw factory in 2024 and ceased the production of complete buses in Europe. Most recently, Alexander Dennis proposed closing its long-standing Falkirk factory in Scotland to focus solely on the production of chassis. These scale-backs result in the loss of skilled jobs, both directly and within the supply chain, with Unite the Union estimating that every job in bus manufacturing multiplies to three to four jobs in the wider supply chain. As such, the contraction of domestic manufacturing capacity risks triggering a wider industrial decline, weakening regional economies and eroding critical skills.

Unlike the US, the UK and Europe are constrained by international trade obligations and subsidy control rules, which limit the ability to mandate that government-funded purchases are made from domestic suppliers. However, in cases where domestic manufacturers are able to meet production demands, governments should arguably be doing more to support national jobs and economics.

Indeed, earlier this year, Euan Stainbank MP led a debate in parliament to advocate for British bus manufacturers. The debate stressed a need to place higher emphasis on the “social value” weighting when procuring new buses to shift outcomes in favour of domestic suppliers. This weighting has historically accounted for just 5% of the decision, but there is an argument to raise it to 30%, placing greater emphasis on factors such as local jobs, training, apprenticeships, and the wider economic benefit.

Likewise, in the European Union, although countries cannot legally mandate “buy domestic” rules for buses, they can still support local manufacturers through indirect policy tools, with tenders weighing in social value, lifecycle cost, cybersecurity, and environmental standards without discriminating by origin. Governments could also provide permitted subsidies for R&D, factory decarbonisation, skills, and production scale-up, aiding European manufacturers in meeting production demands. Such measures could enable public money to be invested domestically, rather than in supporting overseas businesses.

As an example from Asia, South Korea has recently adopted an indirect approach to supporting domestic industry while remaining within open trade frameworks. Rather than imposing restrictions on imports, the government has revised subsidy criteria for electric buses, introducing updated funding guidelines that link subsidy levels to battery performance, particularly energy density. While subsidies of up to 90 million KRW per bus remain available, vehicles equipped with lower energy density batteries receive significantly reduced support. This disproportionately affects many Chinese manufacturers, such as BYD, Higer and Zhongtong, which commonly use lithium iron phosphate battery technology. In contrast, higher-density nickel-cobalt-manganese batteries produced by domestic firms, including LG Energy Solution, SK On and Samsung SDI are more likely to qualify for full subsidies. This policy adjustment makes imported vehicles less competitive without excluding them, while supporting local manufacturers such as Hyundai Motor Company. The case therefore illustrates how governments can use technical standards and subsidy design to influence procurement outcomes.

Crucially, the international policy challenge is not a binary choice between protectionism and open markets. While strict domestic content rules like those seen in the US can anchor supply chains and safeguard industrial capacity, excessive rigidity risks inflating costs and slowing the deployment of new technologies. Meanwhile, fully open procurement systems may deliver short-term cost efficiencies and faster rollout, but can inadvertently hollow out domestic industries and increase long-term strategic dependence on external suppliers.

A more calibrated approach is perhaps needed to combine targeted support for domestic manufacturing with flexible procurement practices that preserve competition and innovation. This could include strengthening social value criteria, investing in industrial capability, and supporting scale-up in emerging technologies, while still allowing access to international suppliers. In doing so, governments can ensure that the transition to zero-emission buses is not only rapid and cost-effective, but also underpinned by resilient, locally rooted supply chains that sustain jobs and economic value over the long term.

To engage further with this topic, listen to our recent Podcast episode on ‘The International Rise of Chinese Buses.’

By Faig Mahmudov

Similar news